Tax season is coming, and it’s crucial for advisors to help clients make smart financial choices. This blog lists essential maximums for the 2026 tax year.

We have gathered some of the most important figures for Financial Planning in 2026 in the below image, read on to understand what it all means.

Key Definition

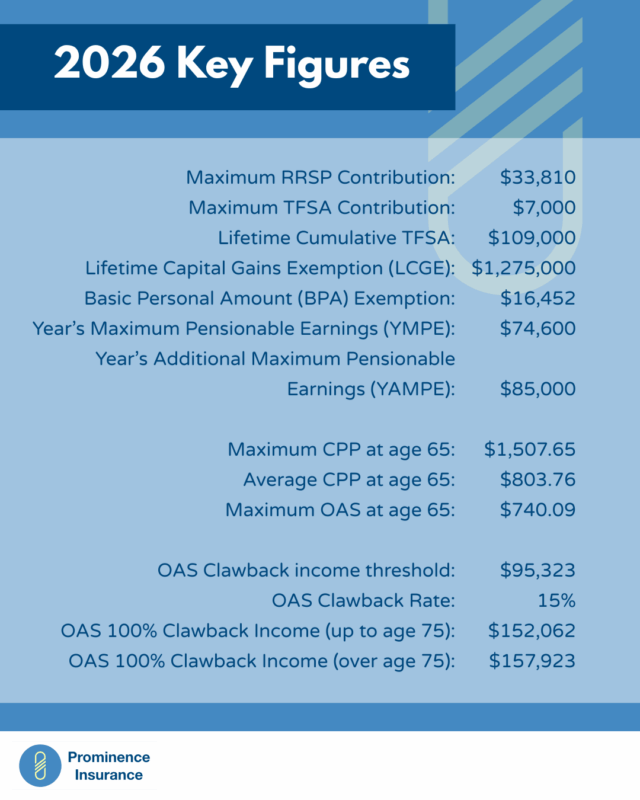

Maximum RRSP Contribution:

This is the max amount an individual can contribute to an RRSP regardless of income within the tax year, this includes personal contribution and group contributions by employers.

The 2026 maximum RRSP Contribution is $33,810.

Maximum TFSA Contributions:

The annual increase in an individual’s TFSA contribution room. This amount is $7,000, same as previous years.

Lifetime Cumulative TFSA:

The maximum TFSA contribution limit for someone eligible since 2009 and never contributed (turn 18 in or before 2009). Previous withdrawals will be added on top of this amount.

The maximum cumulative amount in 2026 will be $109,000.

Lifetime Capital Gains Exemption (LCGE):

The LCGE help individuals shelter capital gains from the sale of qualified small business corporation shares (QSBCS) or qualified farm/fishing property (QFFP). This is for small business owners and their families primarily and does not apply to personal investments like stocks or rental properties. The lifetime Capital Gains Exemption limit in 2026 is $1,275,000.

Basic Personal Amount (BPA) Exemption:

The Federal Basic Personal Amount is the amount anyone can earn without paying federal tax. This is important to keep in mind when discussing how much RRSP contribution may be needed. The 2026 Federal Basic Personal Amount is $16,452. The provincial amount will differ depending on where a person resides.

This amount can decrease for high earners (net income over $258,482 on the federal level).

For older individuals, an additional amount called the federal Age Amount can be claimed. If you are age 65 or older on Dec 31 of the taxation year, the maximum amount you can claim in 2026 is $9,208.

Year’s Maximum Pensionable Earnings (YMPE) & Year’s Additional Maximum Pensionable Earnings (YAMPE):

The Year’s Maximum Pensionable Earnings is the max salary used for CPP contributions, while the YAMPE amount applies for CPP2 contribution. Together they determine the maximum amount of contributions on employment income.

Maximum and Average CPP at Age 65:

The maximum and average CPP payments are not guaranteed, but rather a point of reference. CPP payments received depend on the length of time worked and the contribution made within a person’s lifetime. CPP can also be started earlier or delayed, resulting in an increase or decrease of the payment amount. The 2026 Maximum monthly CPP payment amount is $1507.65, and the average monthly CPP payment amount is $803.76.

CPP is taxable and should be treated the same as employment income.

Maximum OAS at Age 65:

OAS can start at age 65 or be delayed for a higher amount. The maximum OAS at age 65 in 2026 is 740.09. The amount is dependent on the net income of the individual or the household.

OAS is taxable and should be treated the same as employment income.

OAS Clawback Income Threshold:

If your net income exceeds the threshold amount, you must repay part or your entire OAS pension. The 2026 OAS Clawback threshold is $95,233. The OAS Clawback rate is 15%, this is applied on the difference between your income and the threshold amount for the year.

OAS 100% Clawback Income:

The 2026 amount for 100% OAS clawback is $152,062 for individuals up to age 75, and $157,923 for individuals over age 75.

Our Role as Advisors

For many individuals, a key aspect of tax season is understanding RRSP contribution deadlines. Common questions include whether RRSP contributions are necessary, the appropriate amount to contribute, and how an RRSP loan may be beneficial – topics that financial advisors are well-equipped to address.

Furthermore, it is essential for those nearing retirement or already retired to strategically plan withdrawals to minimize personal tax liabilities.

To Summarize

Below is an easy to use table with all the key amounts discussed for quick reference.

| Maximum RRSP Contribution: | $33,810 |

| Maximum TFSA Contribution: | $7,000 |

| Lifetime Cumulative TFSA: | $109,000 |

| Lifetime Capital Gains Exemption (LCGE): | $1,275,000 |

| Basic Personal Amount (BPA) Exemption: | $16,452 |

| Year’s Maximum Pensionable Earnings (YMPE): | $74,600 |

| Year’s Additional Maximum Pensionable Earnings (YAMPE): | $85,000 |

| Maximum CPP at age 65: | $1507.65 / Month |

| Average CPP at age 65: | $803.76 / Month |

| Maximum OAS at age 65: | $740.09 / Month |

| OAS Clawback income threshold: | $95,323 |

| OAS Clawback Rate: | 15% |

| OAS 100% Clawback Income (up to age 75): | $152,062 |

| OAS 100% Clawback Income (over age 75): | $157,923 |

Contact Us

Contact us for more information or Book your FREE consultation using the form below.

By submitting this form, you are consenting to receive marketing emails from: . You can revoke your consent to receive emails at any time by using the SafeUnsubscribe® link, found at the bottom of every email. Emails are serviced by Constant Contact